Conway Twitty, The Twitty Burger, & The Landmark Tax Case That Remains Law Today

Consider yourself lucky if you ever had the opportunity to taste a Twitty Burger, let alone see a franchise. Country Music Hall of Famer Conway Twitty would amass a whopping 44 #1 singles in his illustrious career, would earn millions of dollars in country music, and is arguably one of the most successful artists in country music history. But it was one of his most colossal failures that went on to set an important precedent in American tax code in a landmark case that still remains relevant today, is still regularly taught in both law schools and accounting classes, and had legal professionals giving closing opinions in the pentameter of country songs, if you can believe it.

The case is known as Jenkins vs. Commissioner. “Jenkins” is Harold Lloyd Jenkins—the birth name of Conway Twitty. And “Commissioner” is the commissioner for the IRS.

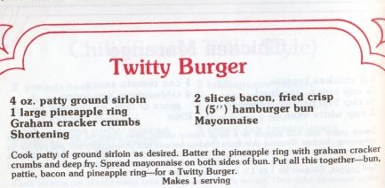

Twitty Burger was first launched in 1968, and included some pretty high-profile investors from country music, including Merle Haggard, Harlan Howard, and Sonny James. What separated the Twitty Burger from other burgers was Conway’s signature burger ingredient: the gram cracker-encrusted pineapple ring that was included on each sandwich. So confident that the pineapple ring would revolutionize the burger business, Conway raised roughly $1 million from his famous country music friends and others as investment capital for the franchise.

But Twitty Burger was doomed from the beginning. Due to poor management, Twitty Burger was not around for very long, and was closed completely by May of 1971. “What I know about is how to make records and how to sing songs, and I’m not too good at anything else, and Twitty Burger is a prime example,” Twitty said.

The “beef” the IRS had with Conway Twitty and Twitty Burger had to do with the famous country singer writing off repayments to his investors on his 1973 and 1974 income taxes. In 1973, Twitty took a $92,892.46 business expense on his taxes, and in 1974, and additional $3,600. The problem the IRS found was these business expenses had to do with Twitty Burger, but were declared under Conway Twitty’s country music earnings.

When Twitty Burger went asunder, Conway decided that the only honorable thing to do was to pay all of his investors back, which he did. The $96,000 he wrote off on his taxes in ’73-’74 was part of those repayments. Twitty and his lawyers argued that if he didn’t repay his debts, it could be detrimental to Twitty’s reputation as a country music singer. That is why it should be permissible to be written off under his entertainment earnings. The IRS disagreed, saying losses from Twitty Burger had nothing to do with country music. So the matter went to court in 1982.

“It was the morally right thing to do,” Twitty insisted. “They put their money in Conway Twitty, and Conway Twitty did it all wrong – that’s why I paid them back.”

What was the result? Conway Twitty won. In 1983, the U.S. Tax court determined that the personal image of country music artists are vital to their careers, and that Conway was in the right to declare the losses to protect his personal reputation. Quotes from country music historians explaining the importance of class in country music were considered by the court in the case.

“We’re fighting over $100,000,” said William Whatley, Conway Twitty’s attorney. “Conway could make that much money in the first three minutes of a concert. It’s the principal that counts.”

Though it’s an interesting snippet of country music history, Jenkins vs. Commissioner is much more significant when it comes to tax matters. The case is still cited as relevant case law even today in how entertainers can declare business expenses on their taxes, and how reputation can factor into decisions.

And this isn’t the only lasting contribution from the case. The court, after deciding in favor of the country legend, rendered their ruling partly in a song called “Ode To Conway Twitty.”

Twitty Burger went belly up

But Conway remained true

He repaid his investors, one and all

It was the moral thing to do.

His fans would not have liked it

It could have hurt his fame

Had any investors sued him

Had any investors sued him

Like Merle Haggard or Sonny James.

When it was time to file taxes

Conway thought what he would do

Was deduct those payments as a business expense

Under section one-sixty-two.

In order to allow these deductions

Goes the argument of the Commissioner

The payments must be ordinary and necessary

To a business of the petitioner.

Had Conway not repaid the investors

His career would have been under cloud,

Under the unique facts of this case

Held: The deductions are allowed.

– – – – – – – –

In 1984, when the IRS decided not to appeal the court’s decision, they responded in kind, saying:

Harold Jenkins and Conway Twitty

They are both the same

But one was born

The other achieved fame.

The man is talented

And has many a friend

They opened a restaurant

They opened a restaurant

His name he did lend.

They are two different things

Making burgers and song

The business went sour

It didn’t take long.

He repaid his friends

Why did he act

Was it business or friendship

Which is fact?

Business the court held

It’s deductible they feel

We disagree with the answer

But, let’s not appeal.

April 18, 2017 @ 7:08 pm

Anyone have the recipe to the twitty burger?

April 18, 2017 @ 7:18 pm

There’s an image of it beside the “Ode to Conway” lyrics, and a video of someone making them at the bottom.

April 18, 2017 @ 7:09 pm

Like pineapple on pizza, I prefer not to have pineapple on my burgers.

April 18, 2017 @ 9:23 pm

Granted I never ate the pineapple burger, but going from the pineapple on pizza yeah I agree with you lol

April 18, 2017 @ 7:16 pm

Graham cracker-encrusted pineapple?

WTF?!?

April 18, 2017 @ 7:16 pm

What an interesting tale. Nothing like a heart warming story for Tax Day.

April 18, 2017 @ 7:26 pm

Striker didn’t crumb the crackers up enough, and he should’ve used Dukes mayo. But, well done none the less.

April 18, 2017 @ 8:27 pm

Great story for tax day!

April 18, 2017 @ 8:29 pm

Interesting. I’d try it.

April 19, 2017 @ 1:47 am

No offense to the great Conway Twitty, but looking at that recipe, that burger kind of sounds like the result of Kenny Chesney and Jimmy Buffet gang banging a Quarter Pounder…

April 19, 2017 @ 2:52 am

if this isn’t an Only in America story, what is

love it, Trig

April 19, 2017 @ 3:53 am

Grilled pineapple and teriyaki sauce on a hamburger is super yummy! Its called a Hula-Burger in Hawaii. Enjoyed the story and it was very fitting as a tax day tome. Three Cheers and a Thousand Twangs to Conway for his honesty and true friendship to his investors.

April 19, 2017 @ 5:52 am

There’s a Merle Haggard/IRS audit story that has a good ending too.

I could go on a rant but I’ll refrain.

April 19, 2017 @ 11:51 am

The Twitty Burger may not be kosher or halal, but any rabbi or iman will tell you that it’s more country than Sam Hunt.

April 19, 2017 @ 12:36 pm

Harold Jenkins was a great man. I am a tax guy and I recall the case. I haven’t heard this in awhile, but back then Conway was called the best friend a song ever had. I have heard from Jimmy Buffett that he credits the inspiration for “Lets Get Drunk and Screw” to many of the lyrics of Conway’s songs.

April 19, 2017 @ 1:35 pm

I’m a tax lawyer by training, and I had forgotten all about this case.

I think there was some Tn state court litigation over Twitty City and his probate estate.